The Map Before the Storm

Is PE Looking at the Right AI Risk?

Scroll down

Introduction

Picture a partners' meeting at a private equity fund in Milan. It is the Q1 2026 portfolio review. The deck is on screen.

One company is ahead of plan: margins are up, and a new client was signed in March. Another is softer than expected: EBITDA is slightly below budget, and management points to a slower sales cycle. A third is on track, with nothing material to flag. Notes are taken. Action points are assigned. Someone mentions a possible add-on. The discussion moves to the pipeline.

It is a normal meeting. Competent people doing competent work. And yet, somewhere in that room, there is a good chance nobody is asking the question that matters most.

Not 'how is the portfolio performing?' but 'how many of these businesses will still have the same moat in three years?' Not 'are our companies becoming more efficient?' but 'are they still structurally defensible in a world where AI is starting to do what they do - faster, cheaper, and without adding headcount?'

The efficiency conversation is already happening. Most PE boardrooms are discussing AI in terms of productivity: faster reporting, automated screening, leaner back-office operations, better analytics. That conversation is real, and it matters.

But it is the easier half of the problem. The harder half is not about processes. It is about business models.

It is about whether the competitive advantage that justified the acquisition, specialised knowledge, human intermediation, proprietary workflows, switching costs, trust, data, relationships, still holds when AI can replicate or replace a meaningful part of it.

That is the question most investment committees and portfolio boards are not yet asking with enough discipline.

The storm is not coming. In several sectors where PE has concentrated significant capital, it has already started. Most boardrooms simply have not looked out of the window yet.

1. Two Questions, Not One

Every business facing AI disruption is really facing two different questions. They sit on different timelines, require different analysis, and lead to different decisions.

The first is a Horizon 1 question: how can AI make the existing business faster, leaner, and smarter? Same product. Same clients. Same business model. Better execution. This is genuine value creation. It is relevant to almost every mid-market company, and it can be addressed within a 12–18-month window in many cases. It is also where most current boardroom discussion sits.

The second is a Horizon 2 question: could AI erode the moat the business was built on? Could a new entrant, a larger competitor, or an AI-native platform replicate or replace the core value proposition at a fraction of the cost? Could the basis of differentiation weaken faster than the company can respond? Could a business that looks efficient today become strategically exposed tomorrow?

If the answer is yes - or even plausibly yes - then the sponsor and management team need to evaluate how the business model should evolve. Not at the next strategy offsite. Not in the next planning cycle. Now.

Horizon 1 is an operational challenge. Horizon 2 is a strategic one.

Confusing the two, or working only on the first while leaving the second unexamined, may become one of the more expensive mistakes a PE board can make in the current environment.

Most Italian PE boardrooms are having the Horizon 1 conversation. Far fewer are having the Horizon 2 conversation with the urgency it deserves. And in at least two sectors where Italian PE has deployed substantial capital over recent years, Horizon 2 risk is no longer theoretical.

It is already moving.

2. Where the Capital Actually Sits

The scale of the exposure becomes clearer when you look at the data.

According to the AIFI-PwC 2025 Italian PE and VC Market Report, around 2,600 Italian companies currently sit in PE portfolios, with a total value at historical cost of approximately EUR 92 billion. In 2025 alone, 887 transactions were completed, representing EUR 11.6 billion invested across the market.

The sector distribution is where the story becomes more interesting.

ICT - the AIFI category covering communications, computers, electronics, software, SaaS, and digital services - accounted for 32% of all PE and VC investments by deal count in 2025. That means 281 transactions, making it the largest sector by a wide margin.

Professional services are harder to map neatly within the AIFI taxonomy. Consulting, accounting, legal, HR, staffing, and broader advisory services cut across several classification categories.

In the past few weeks alone, three notable buy-and-build initiatives in accounting and related services — Spada Partners, SRG Associati and Studitalia — have been announced. Together with other activity across professional services, these deals support the view that private capital is increasingly turning its attention to this segment.

The conclusion is uncomfortable but straightforward. The two areas where Italian PE has deployed an increasing portion of the capital - ICT and SaaS over the last years, professional services more recently- are also two of the areas where AI disruption is most immediate.

This is not a marginal risk sitting at the edge of the portfolio. It is close to the centre.

3. The Sector Map

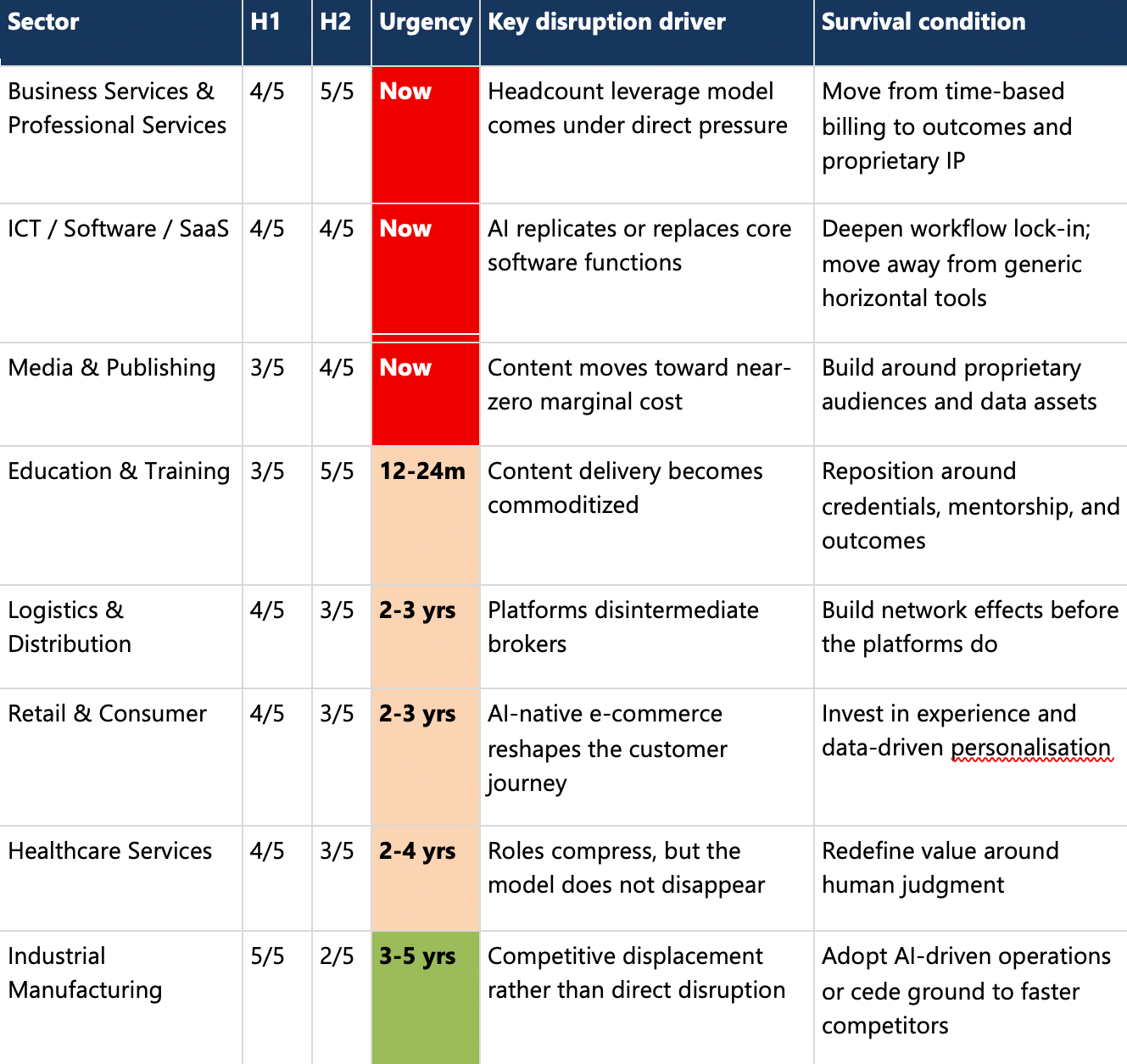

The table below maps the sectors most relevant to Italian PE portfolios across the two horizons.

The H1 score reflects the scale of the AI-driven efficiency opportunity within the existing business model whilst the H2 score reflects the risk that AI disrupts the business model itself.

Urgency indicates how quickly that disruption may materialize in practice.

H1: AI efficiency opportunity within the existing model. H2: AI disruption risk to the business model itself.

Source: Fortlane Partners analysis and research

Three sectors sit clearly in the red: business services, ICT/SaaS, media & publishing. The first two attracted significant capital. Both combine high efficiency potential with high disruption risk. Both require immediate attention.

Education and media also face serious Horizon 2 exposure, although the dynamics are different. Logistics, healthcare, and retail are under pressure too, but the disruption curve is more gradual. There is still time to move, provided the response is deliberate.

Industrial manufacturing is the outlier. It has the largest efficiency opportunity on the list, but lower direct business model disruption risk and a longer runway before competitive displacement becomes acute.

That distinction matters. Not every sector is on the same clock. Part of the work for sponsors is knowing which clock each asset is on.

4. What PE Needs to Do

Recognising the risk is not the same as responding to it. The response needs to happen at three levels: the fund, the due diligence process, and the portfolio company.

4.1 At the fund level

The starting point is to build AI capability that goes beyond general awareness. Funds need a practical framework and operating toolkit that portfolio companies can actually use. That means vendor evaluation standards, data governance guidelines, talent and implementation guidance, and a mechanism for sharing learning across the portfolio. If one company finds an effective approach, the others should not have to start from zero. Over a four-to-six-year hold period, that lost time compounds.

More importantly, funds need an honest view of Horizon 2 exposure across the current portfolio.

The sector map above is only a starting point. Every sponsor should be doing its own version. Which assets are in the red zone? Which are amber? Which genuinely have time? For assets in the red zone, the question is no longer whether to act. It is what to do, and how fast.

4.2 At the due diligence level

AI disruption assessment should become a standard due diligence workstream. Not a footnote in the commercial due diligence report. Not three slides in the technology section. A standalone analysis with its own scope, assumptions, and output.

For business services targets, that means stress-testing the delivery model directly. Which activities generate revenue today? How many of them are replicable by AI at lower cost? What happens to the pricing model if the cost of delivery falls sharply? How defensible is the client relationship if switching costs are lower than they appear?

For ICT and SaaS targets, it means being precise. Vertical SaaS, horizontal SaaS, IT services, managed services, and digital consultancy each carry different exposure profiles. Treating them all as 'tech assets' hides the real risk inside the average. For any target, diligence should also include a direct scan of AI-native competition. Are new entrants already approaching the same customer base with a different cost structure? Are clients beginning to test alternatives? Is the core value proposition becoming easier to replicate than it was two years ago?

A fund acquiring a people-heavy professional services business or a horizontal SaaS platform in 2026 without working through these questions has not finished its diligence. The AI disruption question is now part of the investment decision, whether or not it appears on the standard workstream list.

4.3 At the portfolio company level

The first hundred days of ownership should include a structured AI diagnostic, with two tracks running in parallel.

The Horizon 1 audit maps existing processes against automation potential and identifies the highest-value efficiency initiatives that can begin within ninety days. This is the work most management teams are already prepared to do. It should not wait.

The Horizon 2 audit is harder. It asks management to examine the business model itself also considering the likely evolution of LLM technology soon. What is the company's value proposition built on? Information asymmetry? Human intermediation? Specialist judgment that takes years to develop? Proprietary data? Deep workflow integration? Trust and relationships that are genuinely difficult to replicate? Which of those advantages hold up as AI capabilities improve? And which are more fragile than they look?

For assets in the red zone, that diagnostic should lead to a clear decision. Not a list of options to revisit at the next board meeting. A written response path, with ownership, milestones, and accountability attached.

The market is not waiting for the next board cycle. The storm is not hypothetical and for parts of the Italian PE portfolio, it is already visible on the radar.

ContactGet in touch

What's new?You might also be interested in...