fiberdays 25: Why Germany’s fibre industry is now moving into the “Execution Era”

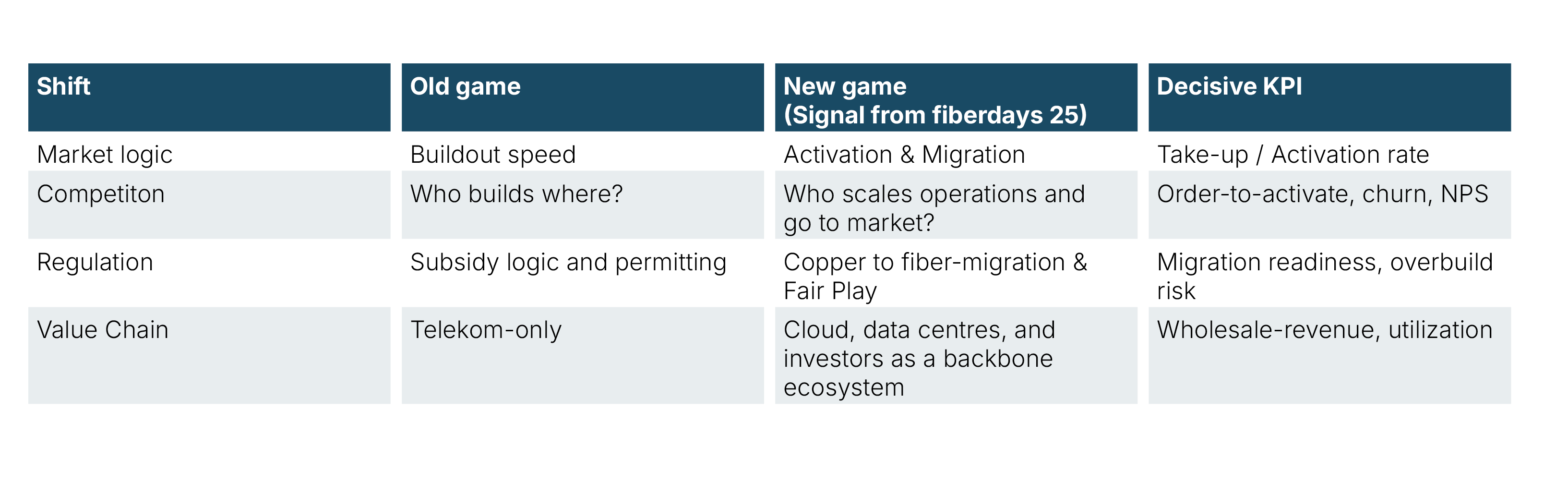

fiberdays 25 signals the shift from build race to execution era: activation, migration, monetisation now define success. Take up, in building readiness, and a frictionless order to activate operating model beat headline homes passed figures. Copper to fibre and truly operable Open Access become the value levers, backed by digital permitting, ESG, and resilience.

Scroll down

Abstract

fiberdays 25 signals the shift from build race to execution era: activation, migration, monetisation now define success. Take up, in building readiness, and a frictionless order to activate operating model beat headline homes passed figures. Copper to fibre and truly operable Open Access become the value levers, backed by digital permitting, ESG, and resilience.

Exec Summary

fiberdays 25 in Frankfurt felt less like a classic trade fair for new components and more like an industry checkpoint. Germany’s fibre rollout clearly has momentum, but the central question is no longer “How fast can we build?” It is: How fast can we activate, migrate, and monetise, without regulating competition to death?

The new guiding theme was visible everywhere. From building to transformation. From homes passed to a homes activated economy. From Open Access as a vision to Open Access as an operating system. And from digitalization as a promise to digitalization as an administrative process (incl. permits, portals, and standards).

Stating the obvious

The biggest topic was fiber again, but with a different tone. The industry is debating its own maturity. If almost half of households are theoretically reachable, but far fewer are actually connected and activated, the bottlenecks are clearly shifting.

Here is the strategic shift that many companies underestimate.

The point is uncomfortable. A built network is not a finished product.

It is a production asset that only delivers returns if (a) households actually switch, (b) in building connectivity is solved cleanly, (c) booking and activation are low friction, and (d) marketing does not end after a single pre-sales push.

That is why copper-to-fiber migration becomes the key question. Without a predictable, consumer friendly, competition neutral framework, copper remains the default network, and fiber keeps fighting inertia, habits, and price anchors. This also explains why Open Access was so present. More providers on one infrastructure can increase activation probability, but only if the operating model works.

Winners & Losers

Strategically, what matters is less “who had the biggest booth” and more “who addressed the right problems”.

Winners (strategic):

- Execution players: Companies that treat fiber as an end-to-end system, from planning to build to activation to operations to customer experience. They invest in process automation, self-service, and standardization, because that is where margin will be created.

- Open Access realists: Not the ones who call for Open Access, but the ones who make it operable, with product catalogues, interfaces, SLA logic, and a clear separation of network and service layers.

- Municipal ecosystems: The focus on municipalities, marketplaces, campus concepts, and best practices is not a nice to have. It is a response to Germany’s biggest constraint, permitting and coordination complexity.

Losers (strategic):

- Build only strategies without an activation plan: Anyone treating buildout as an end will suffer under capital market pressure and competitive dynamics over the next years.

- One size fits all go to market: Pres-sales alone is no longer sufficient. Without continuous, data driven activation programs, network utilization stays too low.

- “Security and ESG later” thinking: Sustainability and resilience move from slides into contracts. If you cannot deliver reporting, energy efficiency, and compliance, you lose tenders, regardless of how strong the technology is.

Hidden Gems

Away from the big panels, there were three details that matter more strategically than they initially appear.

- International carrier exchange and investors view: The strong integration of cloud, carrier, and investor perspectives is a signal. Fiber is being understood as critical infrastructure for cloud, data centers, and AI, not just a consumer access topic. If you can play wholesale, backhaul, dark fiber, and data center connectivity, you move into a larger league.

- Green Plaza: sustainability goes operational: Topics like sustainability reporting, energy and efficiency strategies for data centers, or router refurbishment show that ESG is becoming a cost, risk, and financing factor. This is no longer an image project. It is part of the operating model.

- fibercup and nextgen: The hype around splicing is more than a show. It is a workforce signal. Rollout programmes fail not only on permits, but also on capacity, skills, and quality assurance. Talent pipelines become a competitive factor.

Take-away

fiberdays 25 supports a thesis that companies should now translate into roadmaps.

Thesis 1: Activation beats buildout.

Build activation engines, including in building partnerships, clean processes, clear product logic, and continuous campaigns.

Thesis 2: Open Access needs an operating model.

Define roles, SLAs, interfaces, and product catalogues, and make self-service the default, not a project.

Thesis 3: Copper to fibre is the decisive system bet.

If you do not prepare migration, including communication, pricing, switching processes, and regulatory scenarios, you will remain stuck in parallel structures.

Thesis 4: Digital permitting is a competitive advantage.

Invest in digital planning and permitting processes, GIS integration, standardized line and asset information, and construction ops. This scales faster than adding more build crews.

Thesis 5: ESG and resilience become deal breakers.

Anchor sustainability, energy, security and resilience in architecture and reporting before customers or banks demand it.

If you want to summarize fiberdays 25 in one sentence. Germany’s fiber industry has grown up, now it has to act like an adult.

ContactGet in touch

What's new?You might also be interested in...